How Community Banks Can Win More SME Clients in 2025 (Without Competing on Price Alone)

.png)

The banking industry is facing a new reality: small and medium-sized enterprises (SMEs) have emerged and strong pillars in creating economic stability, and they know it. For many years, they have remained underserved by many financial institutions.

Now, banks are starting to adjust their long-held traditions to focus more on SMEs, but simply adjusting pricing on financial products like loans, credit, or accounts is no longer enough to win loyalty.

The question every bank should be asking is: how can we attract small business banking clients and keep them for the long term?

The answer lies not in a race to the bottom on fees, but in building lasting relationships through innovative solutions, digital banking, and true support for entrepreneurs.

This article explores the strategies that will help community banks gain a competitive edge in 2025 and beyond.

The SME Opportunity in 2025

Across the United States, small and medium-sized enterprises account for more than 99% of all companies. They employ millions of people, fuel local growth, and represent a vital part of every community’s economic fabric.

For banks, they are not only an important customer segment but also a steady source of revenue and opportunities to invest in new services and programs that strengthen long-term relationships.

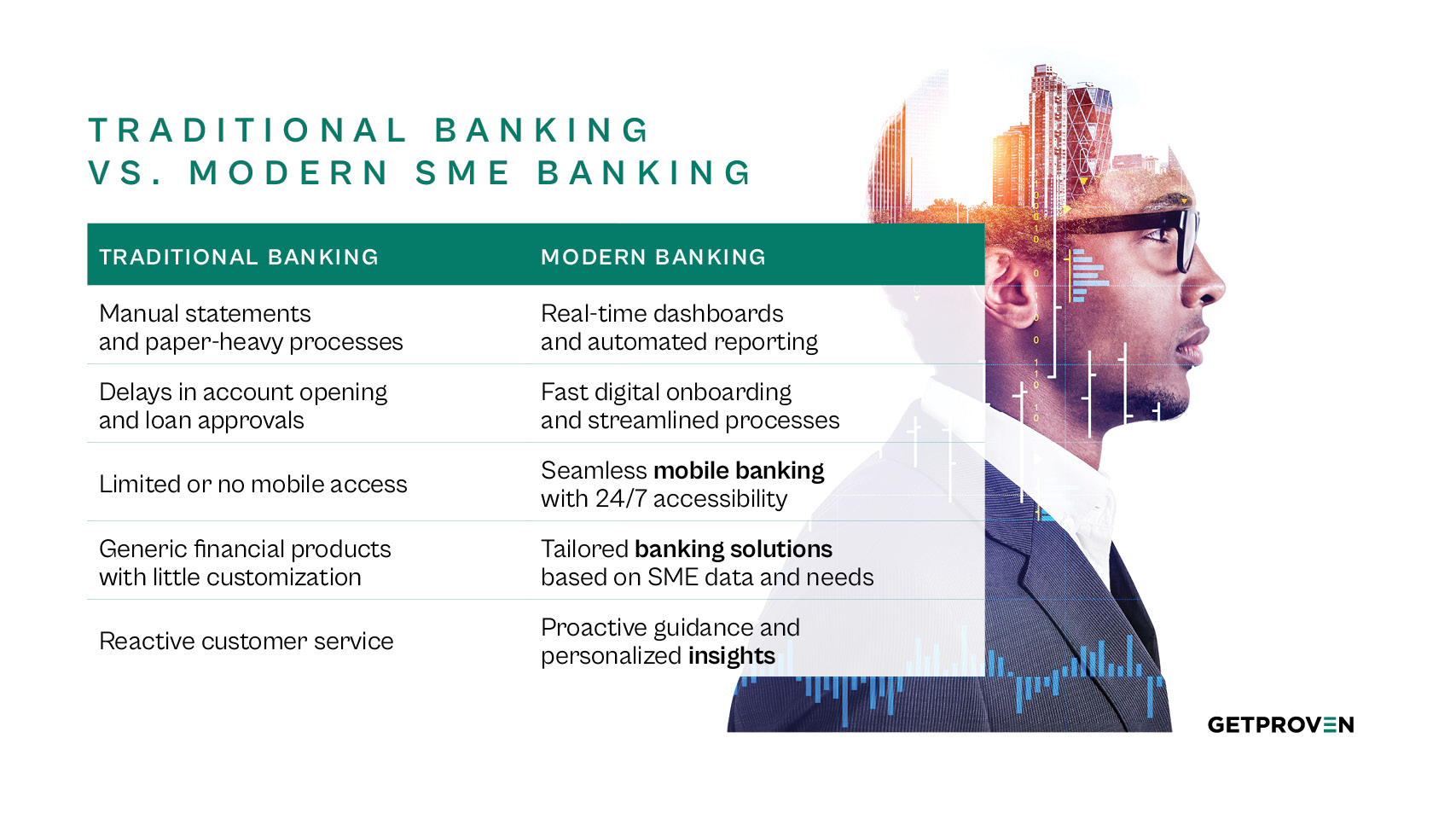

And yet, despite their importance, many SMEs continue to feel overlooked by traditional financial institutions. Business owners frequently cite low customer satisfaction, slow processes, and limited access to modern banking solutions as reasons they struggle to get the support they need.

In practice, this means entrepreneurs spend valuable time wrestling with outdated systems instead of focusing on their core business.

For community banks, this disconnect creates a once-in-a-generation opportunity. By stepping up as true partners in business banking, they can help SMEs manage critical needs like cash flow, payments, and daily operations, while also building the kind of trust that drives loyalty and long-term retention. In 2025, the banks that seize this opportunity will not only secure new clients but also cement their role as enablers of local success.

Some community banks are already experimenting with curated vendor programs to support SMEs. Platforms like Proven make this easy to implement, giving banks a fast way to provide value-added services without adding to their own operational burden. Learn more here.

Why Competing on Price Alone Fails

Lowering loan rates or cutting fees might attract a few new customers, but it rarely ensures long-term success.

Competing only on money:

- Erodes margins and puts banks in a cost war.

- Ignores other factors that drive customer experience, like security, mobile banking, and transparent communication.

- Leaves banks vulnerable to fintech challengers who differentiate with technology, platforms, and real-time insights.

The path forward is to create more value through solutions that go beyond traditional finance.

Top Strategies to Attract and Retain SME Clients

1. Offer Value-Added Services Beyond Finance

For decades, SMEs have expected little more from their banks than financial products such as loans, credit, and accounts. But expectations are shifting. A recent survey of small businesses by the American Bankers Association found that over half of SME owners want banks to provide access to non-financial services—from payroll vendors to HR tools.

Community banks that introduce curated platforms with exclusive vendor deals can immediately demonstrate their commitment to SME success. Imagine a local entrepreneur logging into their digital banking portal and finding discounted accounting software or access to vetted legal services. These extras are not costly for the bank to provide, but they create a visible benefit that competitors often lack.

2. Embrace Digital and Mobile Banking

Digital transformation is no longer optional. According to the FDIC, more than 40% of small business owners consider mobile banking “essential” when choosing a bank. That means that clunky interfaces or slow account setup processes can quickly push a customer to a challenger bank or fintech.

Community banks don’t need to rival the budgets of national players, but they must deliver secure, user-friendly mobile banking and digital banking options. Even incremental improvements like real-time cash flow dashboards or faster payments processing signal to SMEs that their bank is investing in the customer experience.

3. Become a Trusted Advisor

Price competition is transactional. Trust, however, builds loyalty. Research consistently shows that SMEs are more likely to stay with a financial institution that provides insights and guidance, not just credit lines. Deloitte, for instance, has reported that SMEs view banks as one of their top three potential sources of advice on business growth.

Community banks can lean into this by creating practical content, hosting local workshops, and equipping relationship managers with industry-specific knowledge. When a banker helps an entrepreneur make an informed decision about financing equipment or entering a new market, they strengthen the relationship in a way that outlasts any temporary pricing promotion.

4. Use Data and Analytics to Personalize Support

Personalization is becoming a decisive factor in banking customer satisfaction. With analytics and even simple forms of predictive analytics, banks can anticipate what SMEs will need before the client asks for it. For example, a bank that notices seasonal dips in a retailer’s cash flow could proactively offer short-term credit, or provide real-time insights into alternative finance options.

This approach is not about pushing new products, but about enabling SMEs to make better decisions. According to McKinsey, banks that use data-driven personalization see a 10–15% boost in client retention. For community banks competing against larger institutions, this is a low-cost but powerful way to deliver a competitive advantage.

5. Market Proactively to Entrepreneurs

Many community banks still rely on word of mouth and branch traffic to attract new customers. But SMEs increasingly research financial solutions online. Effective marketing campaigns, ranging from targeted digital ads to community-focused case studies, help banks reach entrepreneurs at the right moment.

Highlighting success stories, spotlighting existing SME clients, and showing measurable benefits of banking locally can differentiate a bank from both fintechs and national players. For example, a campaign that shares how a bank helped a local restaurant secure funding and negotiate with suppliers not only attracts business banking leads but also reinforces loyalty among existing customers.

6. Build Trust Through Security and Transparency

Trust remains a deciding factor in choosing a bank. For SMEs, security of data, payments, and accounts is absolutely vital. The rise of cyber threats means banks must go beyond compliance checklists. Transparent communication about security measures, processes, and vendor vetting builds credibility.

Banks that are open about how they protect customer interests, ensure compliance, and choose partners gain a clear competitive edge. In an environment where entrepreneurs feel stretched thin, knowing their banking solutions are both safe and straightforward allows them to focus on running their business, not worrying about fraud or hidden costs.

Who’s Leading the Way?

Across the country, a handful of forward-looking community banks are already showing what’s possible when institutions step beyond traditional boundaries.

One regional bank recently launched a digital platform that connects its SME clients with vetted service providers in areas like payroll, HR, and legal support. For the business owners using it, this means less time searching for reliable partners and more time focusing on running their companies and driving growth.

Others are investing directly in the mobile banking experience, rolling out features that provide real-time insights into a client’s cash flow. Instead of waiting for end-of-month statements, entrepreneurs can now make quicker, more informed decisions about everything from payments to short-term financing needs.

There are also examples of banks leaning heavily into storytelling, using targeted marketing campaigns to spotlight their role in supporting local businesses.

By highlighting success stories such as helping a family-owned restaurant expand or enabling a startup to secure its first line of credit, these banks demonstrate their commitment to the community and gain a visible competitive edge in the process.

Taken together, these cases prove that even relatively small financial institutions can make a big impact. With the right mix of digital tools, value-added services, and authentic communication, community banks can not only compete but thrive in today’s crowded market.

How Banks Can Start Small (Action Plan)

If you're wondering how to attract small business banking clients, the good news is that it doesn’t require a massive overhaul of systems or millions in new technology. In fact, the most effective changes often come from small, deliberate steps that show a clear commitment to supporting business clients.

One of the simplest ways to begin is by offering a curated platform of trusted vendors. Rather than leaving business owners to navigate a sea of options, the bank can step in as a guide, providing access to vetted partners for accounting, payroll, legal, or HR support. A solution like Proven allows this to be implemented quickly, giving SMEs immediate value without the bank needing to build new infrastructure from scratch.

Another area where banks can move the needle is with targeted programs that respond to real SME needs. For example, offering discounted software subscriptions or bundled services for cash-flow management not only supports day-to-day operations but also demonstrates an understanding of the unique challenges entrepreneurs face.

Even the data banks already hold can be put to better use. By analyzing transaction patterns, seasonal revenue cycles, or common payment bottlenecks, banks can surface practical insights that help their clients make more informed decisions. Sharing these findings through personal outreach or digital dashboards signals that the bank is a true partner, not just a place to store money.

Perhaps most importantly, improvements in customer satisfaction don’t always require sweeping changes. Streamlining internal processes, speeding up account openings, and offering more transparent communication can have an outsized effect on how SMEs perceive their banking relationship. These small wins build trust, encourage loyalty, and reinforce the idea that the bank is focused on the client’s success.

Unsure where to start? begin with one initiative, do it well, and let the results compound. Each step taken, whether it’s rolling out a vendor marketplace, enhancing digital touchpoints, or launching a single support program, lays the foundation for stronger relationships, deeper retention, and a clear competitive advantage. Once you prove demand, expand into more robust solutions.

.jpg)

Conclusion

The future of SME banking belongs to the institutions that move beyond transactional thinking. Competing on pricing alone may bring short-term wins, but it does nothing to build the relationships that ensure long-term success.

Community banks have a unique opportunity: to combine local trust with modern digital banking experiences, innovative solutions, and a genuine commitment to helping entrepreneurs thrive. By taking even small steps, whether launching a vendor marketplace, refining mobile banking, or providing sharper insights, banks can transform how SMEs perceive them.

Proven was built for exactly this purpose. As a turnkey platform, it enables banks to deliver SME-focused value without heavy investment in new technology. With Proven, community banks can strengthen loyalty, attract new customers, and secure their role as indispensable partners in local business success.

The banks that thrive in 2025 won’t be the cheapest. They’ll be the ones that deliver the most value.

If your institution is ready to attract new SME clients and strengthen existing relationships, explore how Proven can help. We offer a turnkey way to deliver SME-focused value without overhauling your core systems.

Browse more topics from this article

Heading 1

Heading 2

Heading 3

Heading 4

Heading 5

Heading 6

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur.

Block quote

Ordered list

- Item 1

- Item 2

- Item 3

Unordered list

- Item A

- Item B

- Item C

Bold text

Emphasis

Superscript

Subscript

Heading 1

Heading 2

Heading 3

Heading 4

Heading 5

Heading 6

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur.

Block quote

Ordered list

- Item 1

- Item 2

- Item 3

Unordered list

- Item A

- Item B

- Item C

Bold text

Emphasis

Superscript

Subscript

Heading 1

Heading 2

Heading 3

Heading 4

Heading 5

Heading 6

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur.

Block quote

Ordered list

- Item 1

- Item 2

- Item 3

Unordered list

- Item A

- Item B

- Item C

Bold text

Emphasis

Superscript

Subscript

Heading 1

Heading 2

Heading 3

Heading 4

Heading 5

Heading 6

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur.

Block quote

Ordered list

- Item 1

- Item 2

- Item 3

Unordered list

- Item A

- Item B

- Item C

Bold text

Emphasis

Superscript

Subscript

Heading 1

Heading 2

Heading 3

Heading 4

Heading 5

Heading 6

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur.

Block quote

Ordered list

- Item 1

- Item 2

- Item 3

Unordered list

- Item A

- Item B

- Item C

Bold text

Emphasis

Superscript

Subscript

.png)