Top Reasons SMEs Switch Banks (And How to Stop It)

.png)

For financial institutions, especially community banks and credit unions, one of the greatest challenges is not only winning small business customers but also keeping them. Across the banking industry, customer retention has become a crucial aspect of long-term growth. Attracting new business clients is costly, while retaining existing customers delivers compounding value over time.

Yet many businesses feel underserved by their primary bank. According to multiple surveys conducted over the years, a significant portion of small businesses consider switching banks each year, often citing frustrations with customer experience, outdated banking services, or a lack of personalized financial guidance.

For banks that want to stay in the game, this is a problem that must be solved now more than ever. Understanding why SMEs leave and how to prevent it is key to building stronger long-term relationships.

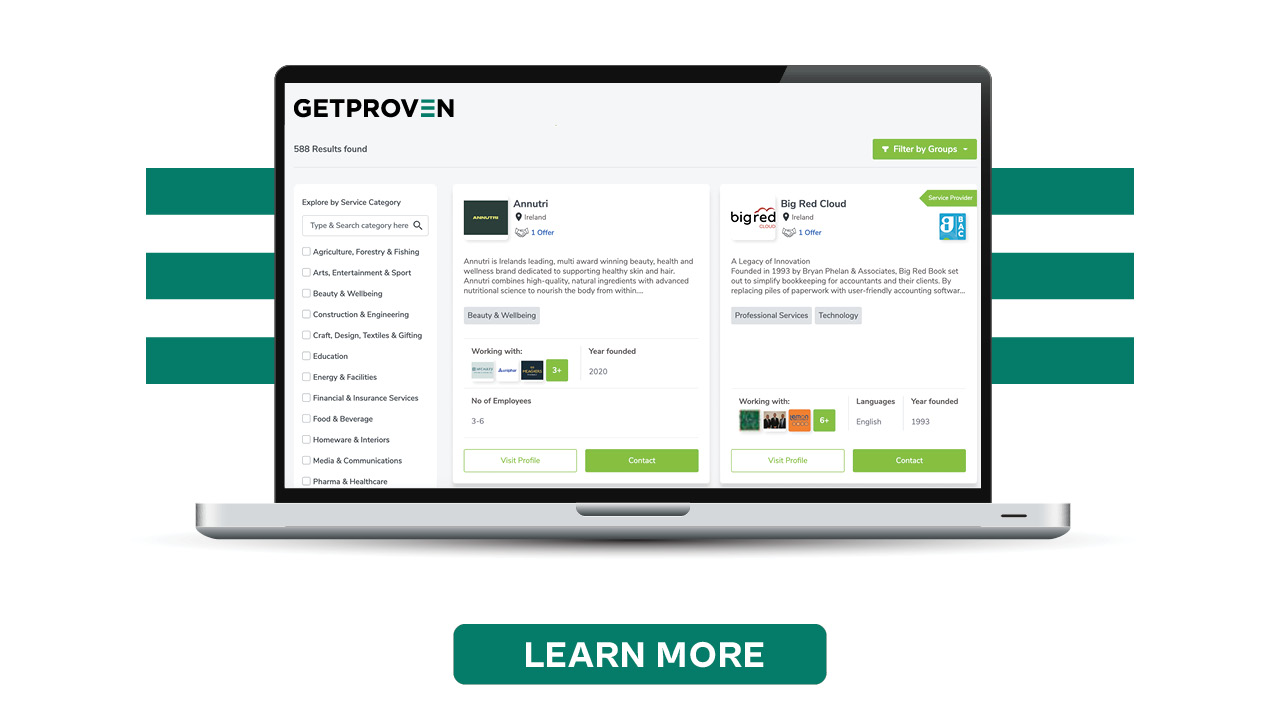

Before we dive in, if you're currently looking for a simple digital platform that can amplify customer retention and align your institution with current customer expectations, explore the Proven platform.

Discover you can improve customer interactions and loyalty for your existing banking customers and even attract new SMEs with our custom-built marketplace of pre-vetted solutions that your prospects need. Learn more here.

The High Cost of Losing SME Clients

When a financial institution loses an SME account, the impact is far greater than the loss of a single relationship. Existing customers typically represent steady deposits, recurring financial transactions, and a constant need for financial services ranging from credit lines and lending solutions to treasury management and international payments.

In practical terms, every departing SME client takes away not only today’s revenue but also tomorrow’s pipeline of opportunities.

Consider the ripple effect: a small manufacturer that leaves its primary bank might also move its payroll, supplier payments, and access to digital banking tools. The bank loses the chance to finance future business operations, provide personalized financial advice, or cross-sell tailored products that improve the client’s financial health.

What’s more, SMEs are highly networked within local communities. When one firm switches providers, others often follow, further weakening the bank’s brand reputation. The cost is not just in missed revenue, but in wasted resources.

In the community, financial institutions are increasingly being forced to spend heavily on marketing campaigns, onboarding processes, and compliance reviews for each new SME relationship. Research consistently shows that attracting a new business account costs five to seven times more than retaining an existing one.

For smaller banks that operate with leaner budgets than national providers, that gap is especially significant.

This is why leading financial service providers place retention at the heart of their growth strategy. By focusing on customer retention in banking, they avoid costly churn, protect their base of loyal customers, and build stronger, more profitable banking relationships over time.

In short, the most reliable path to growth is not chasing new logos; it’s ensuring that current small business clients see long-term value in staying.

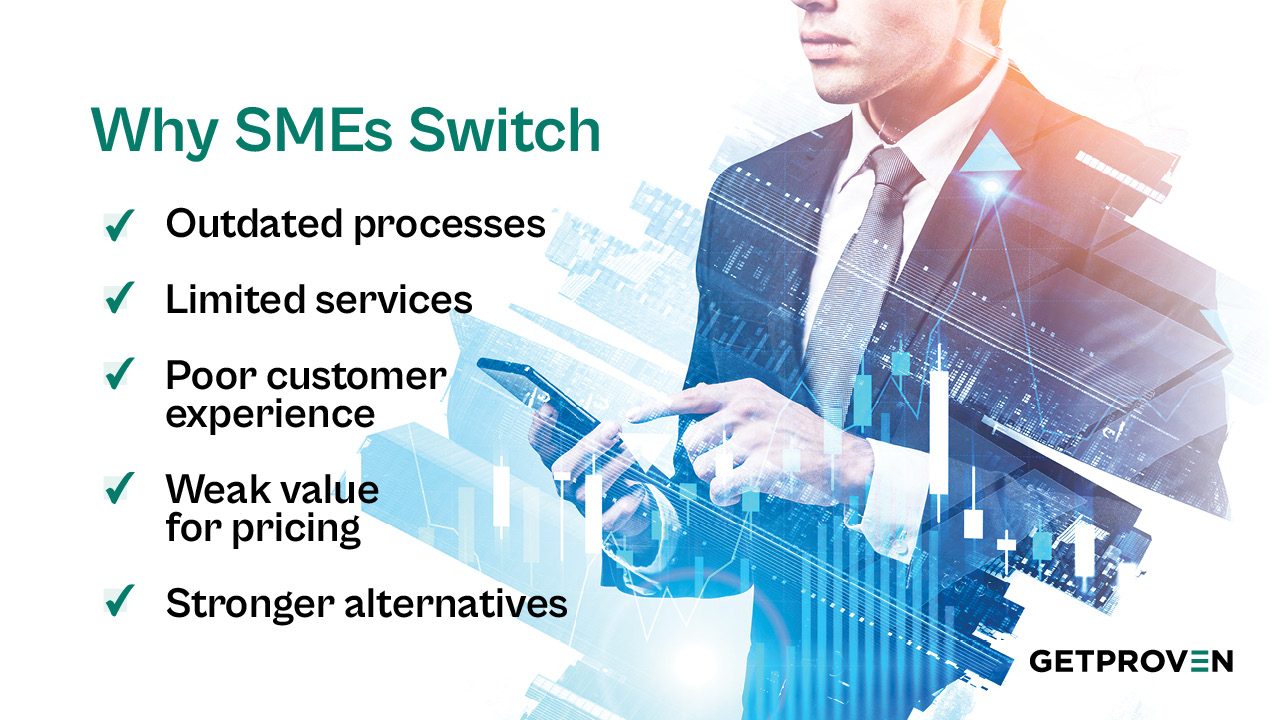

Top Reasons SMEs Switch Banks

While every financial institution knows that customer retention in banking is important, not all understand why small business customers decide to leave in the first place. From the bank’s perspective, churn can feel sudden or unpredictable. But for business clients, the reasons are often clear and they go beyond just competitive pricing.

The truth is that SMEs are facing increasing pressure in today’s fast-changing business landscape. They expect services that are faster, more digital, and better aligned with their day-to-day business operations.

When their banking partner fails to keep up, they start exploring alternatives whether that means larger banks, fintech companies, or other financial service providers.

Understanding these drivers is essential for community banks, credit unions, and other banking providers who want to retain customers and strengthen long-term relationships. Here are the most common reasons SMEs switch, and what they mean for your institution.

1. Outdated Processes and Lack of Digital Transformation

For small business owners, time is money. Unfortunately, many traditional banks still rely on manual processes that slow down routine tasks like account opening, loan applications, or international payments.

Entrepreneurs who run lean operations don’t have hours to wait in branches or days for approvals. They want fast, frictionless solutions.

This is where digital banking makes all the difference. Fintech companies and innovative financial service providers have reset the bar with sleek mobile apps, cloud computing capabilities, and seamless digital experiences that provide valuable insights in real time. When SMEs experience these alternatives, they begin to view outdated systems as unacceptable.

Your takeaway: without embracing digital transformation, the institution risks losing clients to providers offering faster, smarter, and more secure banking services. It's not a 'maybe', it's already happening.

2. Limited Service Offerings Beyond Traditional Banking Services

Historically, banks focused on financial products like credit lines, loans, and deposit accounts. While these remain essential, today’s SMEs expect more.

They need banking partners who understand the complexities of modern business and can provide tools to manage everything from accounting software to financial management.

Increasingly, SMEs want banks to act as one-stop financial partners, offering tailored financial products alongside digital solutions that integrate with their day-to-day operations. Without this, entrepreneurs are left seeking out other solutions like fintech alternatives that can deliver the breadth of service offerings they demand.

Forward-thinking community banks are starting to address this by creating curated ecosystems that connect clients to payroll firms, legal advisors, or international markets through digital platforms. This approach doesn’t just fill a gap; it positions the bank as a primary financial institution that supports long-term relationships.

3. Poor Customer Experience and Weak Communication

SMEs are often promised superior customer service from their banking providers, but the reality often falls short. Many banks struggle with slow response times, rigid policies, and inconsistent communication.

For small business owners, these gaps translate into frustration and a perception that their banking relationships are transactional rather than supportive.

Even more damaging is the lack of personalization.

Entrepreneurs want personalized financial guidance and customer insights that help them make informed decisions about financing, management, or expansion into new markets. When a bank doesn’t step up with valuable insights or proactive outreach, SMEs question the value of remaining with that institution.

In contrast, institutions that combine high-quality services with consistent, transparent communication strengthen customer satisfaction and drive customer loyalty. The new opportunity is to shift positioning and become trusted advisors instead of vendors selling products.

4. Pricing Without Perceived Value

Many banks fall into the trap of believing that competitive pricing is enough to retain customers. But small businesses don’t always choose the cheapest provider. They choose the one that delivers the most value.

If fees for banking services increase without added benefit, or if financial products like loans and credit lines feel commoditized, SMEs are quick to explore other potential banking partners.

Research shows that business owners are often willing to pay slightly more for banking solutions that come with superior customer service, digital solutions, and personalized financial guidance. In other words, it’s not about being the cheapest option in the marketplace; it’s about demonstrating clear, everyday value that justifies the cost.

Banks that focus exclusively on lowering prices risk commoditization and eroded margins. Those that instead create service offerings tied to real business outcomes, including helping SMEs manage financial health, improve financial operations, or gain customer insights, win lasting loyalty.

5. Stronger Alternatives in the Market

The rise of fintech companies and digital-first financial service providers has given SMEs more choice than ever. These new entrants combine sleek mobile banking tools, strong data security, and integration with everyday business operations. They also leverage advanced technology like predictive analytics to deliver personalized financial advice at scale.

For a small business owner, this is a very attractive proposition. It's faster service, smarter insights, and a banking partner that feels aligned with their needs. Compared to that, many traditional banks appear slow-moving and inflexible.

If your bank doesn’t adapt, it risks losing not only loyal customers but also its relevance and position in the ecosystem of local businesses.

To remain competitive, the institution must embrace digital transformation, expand its service offerings, and lean into the strengths that fintechs can’t replicate, namely local trust, community presence, and authentic customer relationships.

How to Stop the Churn

The good news is that high churn rates are not inevitable. SMEs don’t want to jump from one provider to the next. They are, in fact, looking for a partner they can trust, one that understands their needs and delivers real value. Here's how your institution can position itself as that partner.

1) Embrace Digital Transformation

Today’s consumers live in a digital-first world. Your SME clients are no exception. They expect a seamless digital experiences across online banking, mobile apps, and core banking services.

A bank that still relies on paper-heavy onboarding or manual loan applications risks losing credibility with SMEs who already rely on fintech companies for speed and simplicity.

By investing in digital solutions, whether that’s cloud-based platforms, tools for predictive analytics, or mobile features that track financial health, banks can meet rising customer expectations. These tools not only improve customer satisfaction but also give entrepreneurs valuable insights into their financial operations, strengthening the case to stay loyal.

2) Go Beyond Basic Services

Business owners need more than a place to deposit funds or take out a loan. They’re looking for a partner who understands the realities of running a company day to day. That might mean help with payroll, access to reliable accounting tools, or guidance on reaching new markets.

Forward-looking banks are responding by creating ecosystems of support by bringing in trusted vendors, consultants, and technology partners to fill those gaps. With solutions like Proven, it’s possible to launch a curated resource hub quickly, giving small businesses access to tools that make life easier. Banks that take this approach move from being just another provider to becoming a central partner in their clients’ success.

Some forward-thinking banks using this opportunity to build new ecosystems by partnering with vendors, consultants, and technology platforms.

For example, Proven enables banks to launch a curated SME vendor marketplace in weeks, giving clients access to resources that support their daily needs. This kind of innovation positions the bank as a hub that goes beyond transactions to provide end-to-end support.

3) Focus on Relationships, Not Just Products

For entrepreneurs, a loan or a checking account is only part of the picture. What they value even more is a banking partner who understands their business and offers guidance when decisions get tough. Too often, though, banks treat small businesses as identical accounts rather than unique companies with distinct goals and challenges.

By taking the time to understand each client and sharing clear, practical advice(whether it’s managing cash flow, planning for growth, or navigating new markets), banks can show they are more than just service providers. When that advice is paired with responsive service and honest communication, it builds the kind of trust that turns everyday customers into long-term partners.

4) Make Security a Source of Confidence

As more business activity moves online, protecting sensitive data is no longer optional. Small businesses want to know their information is safe and that their bank is serious about compliance. One breach or misstep can undo years of trust and push loyal clients toward competitors.

Community banks can turn this risk into a strength. By being transparent about safeguards, investing in modern protections, and showing clients how their data is secured, they can reassure entrepreneurs that their financial operations are in good hands. Strong security combined with open communication sends a clear signal: this is a partner you can trust.

When banks commit to modernization, broaden their support beyond core services, offer proactive guidance, and back it all with strong security, they address the very issues that drive businesses away. More than that, they reposition themselves as forward-looking partners; providers of not just money, but of stability, insight, and confidence in a fast-changing world.

Conclusion

SMEs rarely leave their bank because of a single fee increase or isolated frustration. More often, churn is the result of a broader mismatch between client expectations and what their financial partners deliver.

Outdated banking services, limited service offerings, poor customer experience, and stronger alternatives from fintech companies combine to push loyal clients to consider switching banks.

The opportunity for any community-based financial institution lies in reversing this cycle. By developing strong customer retention strategies that leverage technology, expanding beyond traditional banking services, providing personalized solutions, and reinforcing data security, banks can build stronger customer relationships that last for years.

In doing so, they not only protect existing revenue streams but also position themselves as indispensable banking partners in an increasingly competitive financial landscape.

For banks ready to take practical steps, the path forward doesn’t have to be overwhelming. Platforms like Proven give institutions a simple way to add value, connect SMEs with trusted vendors, and strengthen customer loyalty, all without the cost and complexity of building new systems from scratch.

Ultimately, small business banking isn’t just about holding on to existing customers; it’s about creating lasting, long-term relationships that drive mutual growth, success, and resilience in a rapidly changing market.

Browse more topics from this article

Heading 1

Heading 2

Heading 3

Heading 4

Heading 5

Heading 6

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur.

Block quote

Ordered list

- Item 1

- Item 2

- Item 3

Unordered list

- Item A

- Item B

- Item C

Bold text

Emphasis

Superscript

Subscript

Heading 1

Heading 2

Heading 3

Heading 4

Heading 5

Heading 6

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur.

Block quote

Ordered list

- Item 1

- Item 2

- Item 3

Unordered list

- Item A

- Item B

- Item C

Bold text

Emphasis

Superscript

Subscript

Heading 1

Heading 2

Heading 3

Heading 4

Heading 5

Heading 6

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur.

Block quote

Ordered list

- Item 1

- Item 2

- Item 3

Unordered list

- Item A

- Item B

- Item C

Bold text

Emphasis

Superscript

Subscript

Heading 1

Heading 2

Heading 3

Heading 4

Heading 5

Heading 6

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur.

Block quote

Ordered list

- Item 1

- Item 2

- Item 3

Unordered list

- Item A

- Item B

- Item C

Bold text

Emphasis

Superscript

Subscript

Heading 1

Heading 2

Heading 3

Heading 4

Heading 5

Heading 6

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur.

Block quote

Ordered list

- Item 1

- Item 2

- Item 3

Unordered list

- Item A

- Item B

- Item C

Bold text

Emphasis

Superscript

Subscript

.png)