Stablecoins vs Tokenized Deposits for Banks: What’s the Difference?

If you’re leading strategy, treasury, or product inside a bank right now, you’ve probably heard the terms stablecoins and tokenized deposits used almost interchangeably. They’re often grouped together in discussions about digital assets, faster payments, or the next phase of programmable money.

But when you move from industry panels into an actual internal planning meeting, the distinction between stablecoins vs tokenized deposits for banks becomes much more practical.

The difference affects your balance sheet, your liquidity profile, your regulatory posture, and how examiners will view what you are building. It also shapes how you think about rewards, payments, and customer engagement over the next decade.

This is not an abstract technology question. It is a structural one.

If you’re evaluating how stablecoin activity intersects with regulation and supervision, we covered the broader implications of the GENIUS Act for banks in a separate executive briefing.

Why Does This Distinction Matter Now?

The conversation has accelerated due to policy developments such as the GENIUS Act in the United States and MiCA in Europe. At the same time, fintech competitors and large banks are exploring programmable payments, tokenized assets, and new digital representations of money on public blockchains.

Community banks, regional and community banks, and even credit unions are being asked whether they should operate in this space. Institutional clients are asking about cross-border, international, and real-time payments that move faster than traditional payment rails.

Before deciding how to respond, it helps to understand what exactly you would be adopting.

What Are Payment Stablecoins?

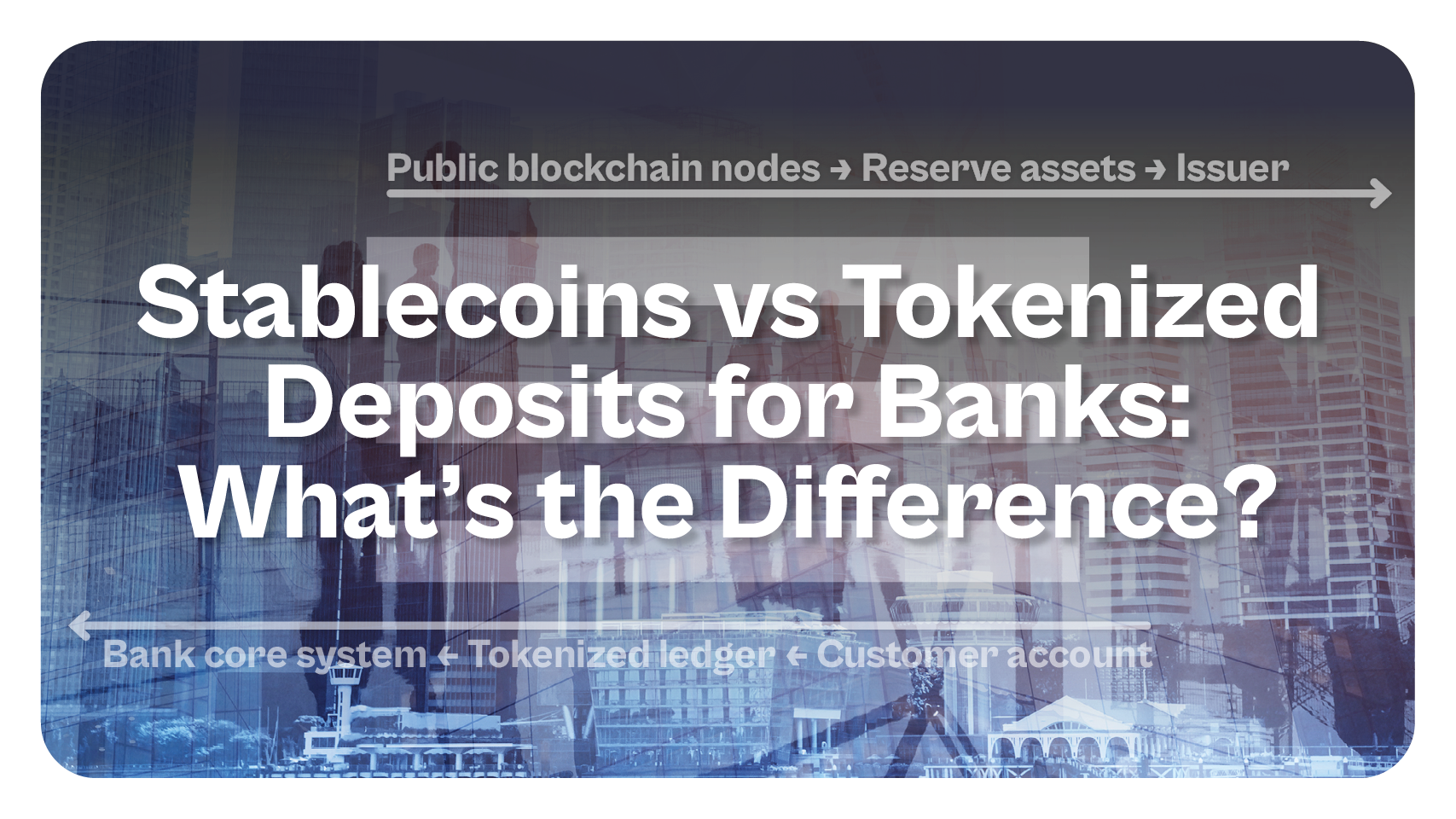

Payment stablecoins are digital tokens designed to represent a unit of currency, usually the U.S. dollar. Most stablecoins are issued by non-bank stablecoin issuers that hold reserves backing those tokens. Those reserves are often made up of treasury bills, cash, or other high-quality liquid assets.

Stablecoins sit outside the traditional banking system. They are not traditional deposits. They are not commercial bank money created through bank lending. They are claims on the issuer’s reserves.

Under emerging regulation, including discussions tied to the GENIUS Act, a permitted payment stablecoin issuer would be subject to defined capital, reserve, and disclosure requirements. Still, even with regulatory clarity, these instruments are not the same as bank deposits backed by FDIC insurance.

Stablecoin holders rely on the issuer’s ability to maintain reserves and honor redemptions. If the issuer manages reserves conservatively in treasuries or other liquid assets, redemption risk may be lower, but it remains structurally different from holding funds inside regulated banks.

In simple terms, stablecoins are a parallel form of digital value that interacts with the financial system but does not sit directly on a bank’s balance sheet.

What Are Tokenized Deposits?

Tokenized deposits, by contrast, are traditional deposits represented in tokenized form. They are issued by regulated banks and remain liabilities of the bank. They continue to be covered by deposit insurance where applicable, and they remain subject to oversight from federal agencies and state regulators.

If a bank tokenizes deposits, it is not creating a new form of money. It is creating digital representations of existing deposits. Those deposits still sit on the bank’s balance sheet. They still support bank credit and bank lending. They remain part of the institution’s liquidity modeling and capital planning.

From a regulatory framework standpoint, tokenized deposits remain inside the banking system. They are commercial bank money in digital tokens rather than in traditional ledger entries. That distinction matters deeply to regulators because it preserves supervisory visibility.

In other words, tokenized deposits modernize the delivery mechanism. They do not change the underlying liability.

The Structural Differences Between Stablecoins and Tokenized Deposits

When comparing stablecoins and tokenized deposits, the most important difference is who bears the liability and where the funds sit.

With payment stablecoins, the issuer holds reserves. Those reserves are typically invested in treasuries or other low-risk assets. The token circulates on public blockchains or private networks, and settlement can happen outside the core banking rails.

The stablecoin does not directly expand or contract a particular bank’s deposits unless customers move funds in or out of their accounts to acquire it.

With tokenized deposits, the liability remains the bank’s. Deposits continue to fund lending. They remain part of treasury management and liquidity calculations. From the standpoint of the Federal Reserve Bank or other regulators, the exposure is familiar because it lives within the traditional supervisory perimeter.

For community financial institutions, this distinction becomes a key differentiator. Stablecoins introduce an external issuer dynamic. Tokenized deposits keep the activity within regulated banks.

Why Regulators Treat Them Differently

Regulators care about systemic risk, deposit flight, and the stability of the financial system. If large volumes of funds move from traditional deposits into instruments that can pay interest or pay yield outside the banking system, that can affect liquidity and credit availability.

This is why discussions around whether stablecoins can pay interest are sensitive. If a stablecoin begins to look like an alternative to traditional deposits, the implications reach beyond payments. They touch bank liquidity, capital planning, and even bank lending.

Tokenized deposits, on the other hand, do not create a new funding channel. They preserve the bank’s liabilities within the regulated framework. That continuity is important for regulators evaluating risk, capital, and liquidity across institutions.

For banks considering whether to issue payment stablecoins or explore tokenized deposits, the regulatory posture is not the same. One introduces an issuer model outside traditional deposits. The other modernizes deposits without altering their core treatment.

What This Means for A Bank's Strategy

For large banks with global operations, stablecoin activities may align with cross-border payments or institutional settlement use cases. For regional and community banks, the calculus is often different.

Issuing or partnering with a stablecoin issuer may introduce new oversight expectations, AML controls, and reserve transparency requirements. It may also raise questions about how such activities interact with the bank’s funding base.

Tokenized deposits may offer faster payments, programmable payments through smart contracts, and improved settlement efficiency without changing the structure of the bank’s liabilities. However, they still require careful integration into existing systems and controls.

The real strategic question is not which technology sounds more innovative. It is which structure aligns with your institution’s balance sheet, liquidity profile, and long-term business model.

How This Impacts Rewards and Incentives

When banks explore stablecoin rewards or other digital incentives, the structural difference matters.

For a deeper look at how banks can design incentive programs without introducing interest mechanics or funding complexity, see our analysis on how banks can reward customers without paying yield.

If a reward design begins to rely on a token that pays interest or behaves like a substitute for deposits, it may raise questions about funding and supervisory interpretation. If incentives are tied directly to balances in tokenized form, they remain part of traditional deposit economics.

A different path is to design rewards that do not depend on interest mechanics at all. Vendor-backed savings, structured discounts, and operational benefits for customers can deliver value without changing how funds sit on the balance sheet.

That separation allows banks to leverage digital innovation without blurring the line between incentives and funding structures.

Looking Ahead

Over the next decade, we are likely to see multiple forms of digital money coexist. Stablecoins, tokenized deposits, tokenized treasuries, and other tokenized assets may all operate in parallel. Big banks may experiment with one structure, while community banks choose another.

The institutions that move carefully will focus less on trending headlines and more on the underlying structure. They will evaluate how each option affects liquidity, capital, supervisory relationships, and the bank’s ability to support lending and credit in their communities.

Technology will evolve, and regulation will continue to adapt. But the core responsibility of banks remains the same: to protect deposits, manage risk, and serve customers in ways that strengthen the broader financial system.

Understanding the structural difference between stablecoins and tokenized deposits is a necessary first step before deciding how to participate in that future.

If your institution is exploring programmable value, rewards, or digital incentives, the next step is to ensure the structure aligns with your balance sheet and supervisory expectations. See how Proven helps banks deliver compliant, non-deposit rewards without altering funding mechanics.

Frequently Asked Questions

1. Are tokenized deposits the same as stablecoins?

No. Tokenized deposits are digital representations of traditional bank deposits issued by regulated banks. They remain liabilities on a bank’s balance sheet and are subject to deposit insurance and supervisory oversight. Stablecoins are typically issued by non-bank stablecoin issuers and backed by reserves such as treasury bills or other high-quality liquid assets. They sit outside the traditional deposit framework.

2. Are tokenized deposits covered by FDIC insurance?

If the underlying deposit qualifies for FDIC insurance, tokenized deposits representing that deposit would generally retain that coverage because they are simply a digital form of traditional deposits. Stablecoins do not carry FDIC insurance unless explicitly structured within a regulated banking framework.

3. Do stablecoins reduce bank deposits?

They can. If customers move funds from bank deposits into payment stablecoins, that can affect liquidity and funding levels. The degree of impact depends on scale, customer behavior, and how stablecoin reserves are structured. For community banks, even moderate deposit shifts can influence liquidity planning.

4. Can banks issue stablecoins directly?

Under proposed regulatory frameworks, such as discussions around the GENIUS Act, banks may be able to issue payment stablecoins if they meet defined capital, reserve, and compliance requirements. However, issuing stablecoins introduces additional regulatory expectations and oversight compared to managing traditional deposits.

5. Do tokenized deposits change how banks lend?

Not structurally. Because tokenized deposits remain traditional deposits in digital form, they continue to support bank lending and credit creation just like other deposits. They do not remove funds from the banking system the way external instruments might.

6. Why are regulators more cautious about stablecoins?

Regulators focus on financial stability, liquidity, and systemic risk. If stablecoins grow large enough to compete directly with traditional deposits or begin to pay interest in ways that shift funding patterns, regulators will evaluate how that affects the broader financial system and credit availability.

7. Should community banks prioritize tokenized deposits over stablecoins?

There is no universal answer. For many community financial institutions, tokenized deposits may align more closely with existing supervisory structures and balance sheet management. Stablecoin participation may require additional resources and regulatory coordination.

8. How does this distinction affect customer rewards programs?

If rewards are tied to interest-bearing digital tokens, they may raise questions about deposit substitution and regulatory interpretation. Incentive models that are structurally separate from deposit balances and funding mechanics tend to move through governance processes more smoothly.

9. Are stablecoins primarily a payments innovation?

They are often positioned as a payments solution, especially for cross-border payments and faster settlement. However, at scale, their impact can extend into funding, liquidity, and deposit dynamics. That is why the structure matters.

10. What should banks evaluate before launching stablecoin-related products?

Banks should assess how the product affects their balance sheet, liquidity modeling, regulatory reporting, and supervisory relationships. They should also consider whether the structure aligns with long-term strategy rather than short-term competitive pressure.

Browse more topics from this article

Heading 1

Heading 2

Heading 3

Heading 4

Heading 5

Heading 6

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur.

Block quote

Ordered list

- Item 1

- Item 2

- Item 3

Unordered list

- Item A

- Item B

- Item C

Bold text

Emphasis

Superscript

Subscript

Heading 1

Heading 2

Heading 3

Heading 4

Heading 5

Heading 6

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur.

Block quote

Ordered list

- Item 1

- Item 2

- Item 3

Unordered list

- Item A

- Item B

- Item C

Bold text

Emphasis

Superscript

Subscript

Heading 1

Heading 2

Heading 3

Heading 4

Heading 5

Heading 6

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur.

Block quote

Ordered list

- Item 1

- Item 2

- Item 3

Unordered list

- Item A

- Item B

- Item C

Bold text

Emphasis

Superscript

Subscript

Heading 1

Heading 2

Heading 3

Heading 4

Heading 5

Heading 6

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur.

Block quote

Ordered list

- Item 1

- Item 2

- Item 3

Unordered list

- Item A

- Item B

- Item C

Bold text

Emphasis

Superscript

Subscript

Heading 1

Heading 2

Heading 3

Heading 4

Heading 5

Heading 6

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur.

Block quote

Ordered list

- Item 1

- Item 2

- Item 3

Unordered list

- Item A

- Item B

- Item C

Bold text

Emphasis

Superscript

Subscript

.png)